The Continued Rise of Premiumization In The Bev-Alc Industry

Premiumization has been an ongoing trend in the industry for the better part of two decades, however, the COVID-19 pandemic has accelerated its march to become the standard-bearer across all bev-alc categories: beer, wine and spirits. While the case can be argued for a slowdown due to a potential looming recession, it’s impossible to ignore the fact that more and more consumers prefer premium products, consequently influencing supplier and distributor portfolios and ultimately on- and off-premise buying behavior.

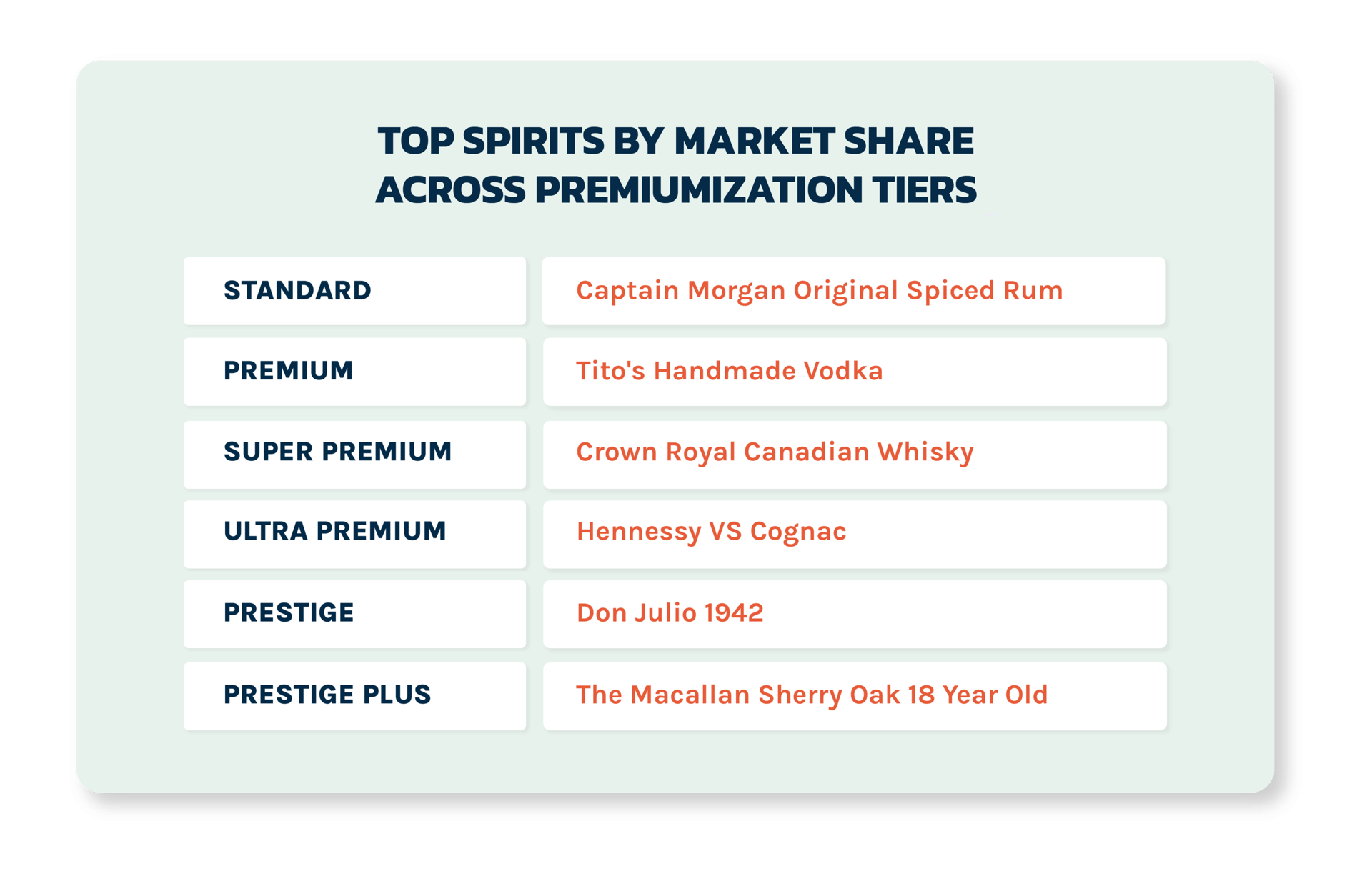

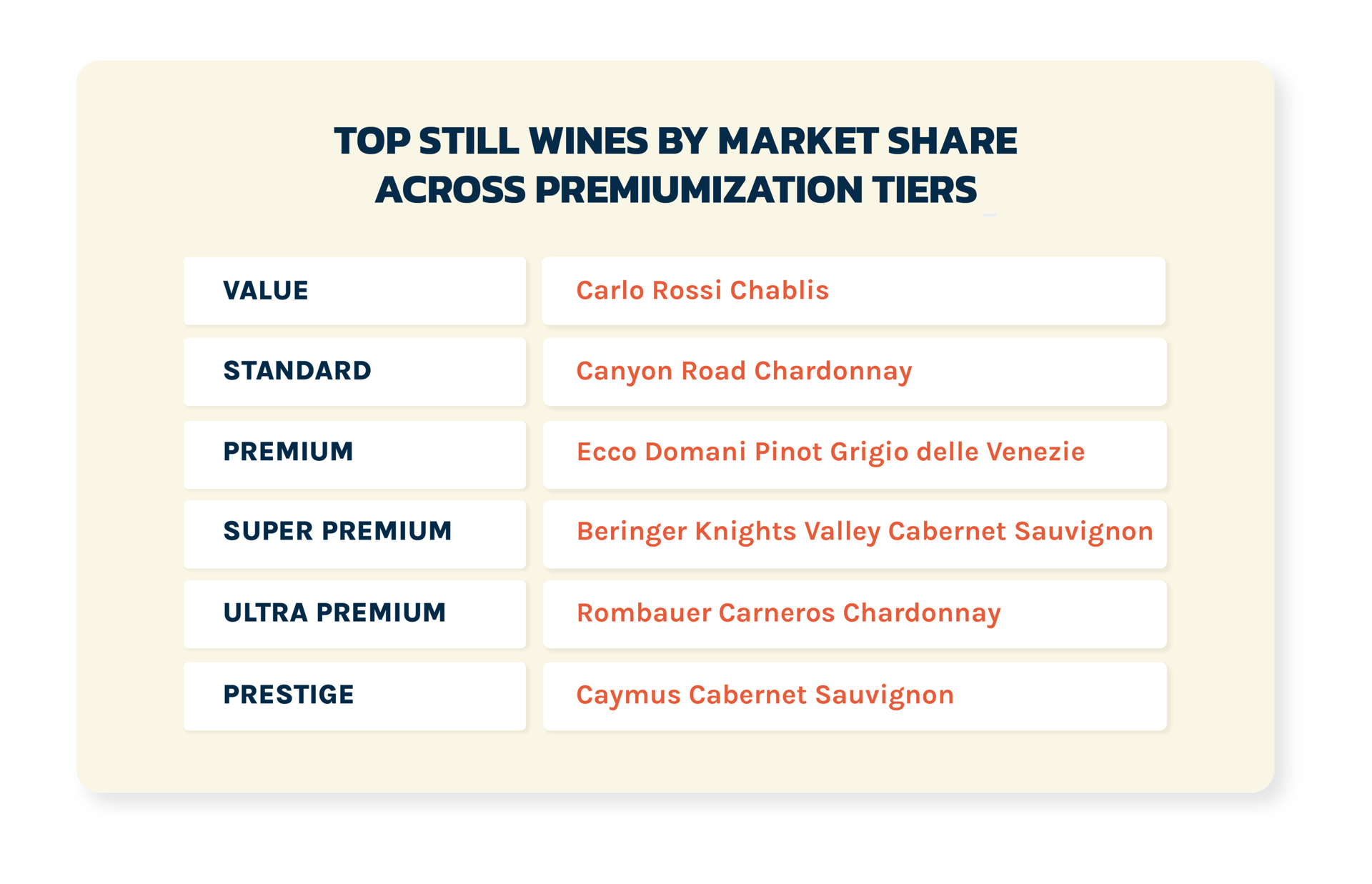

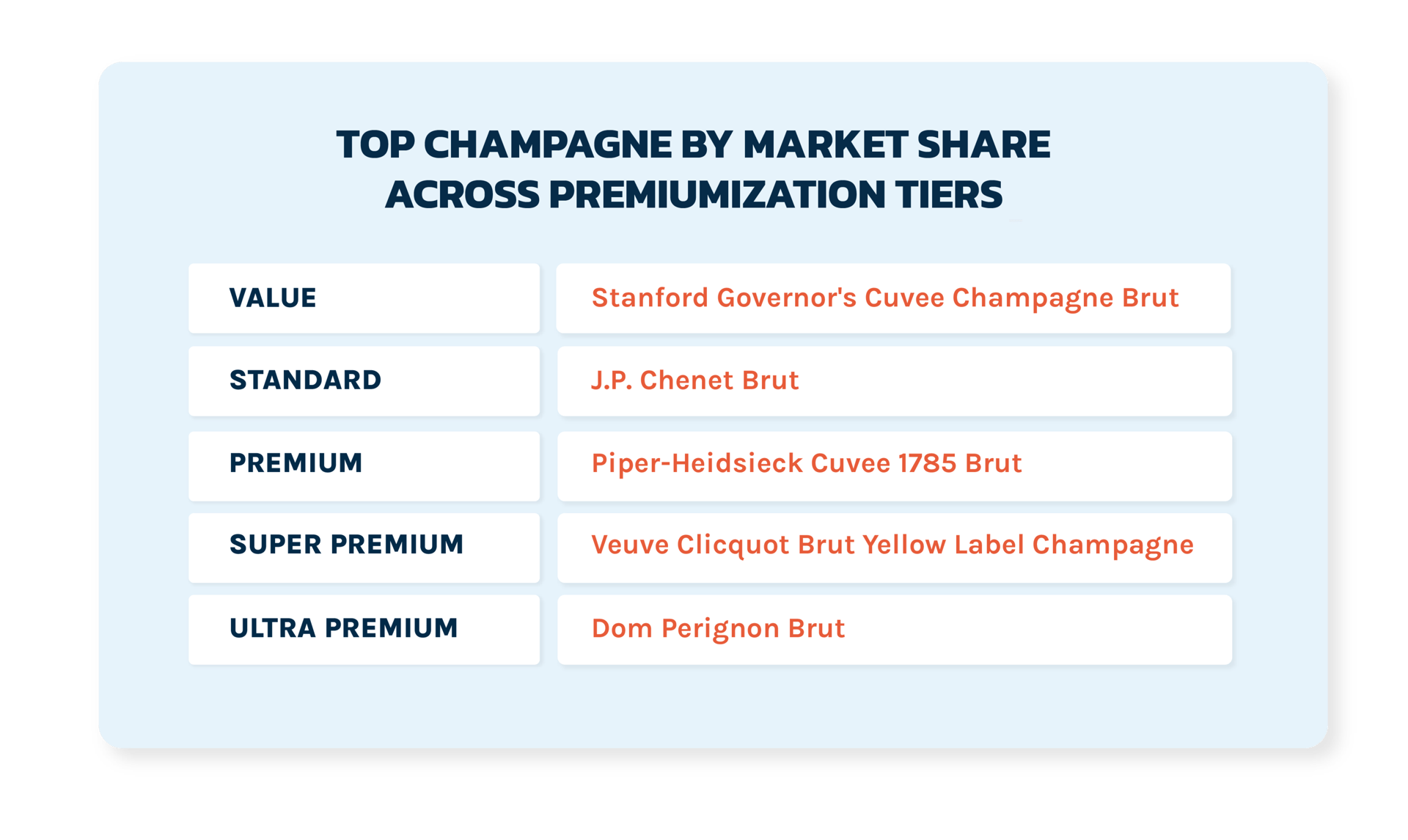

Tiered premiumization price classifications are as defined by IWSR | 2019 US Beverage Alcohol Review

Methodology, Sources & Definitions (Page 14-15). As Provi uses frontline distributor pricing only, we arrived at the dataset by calculating listed IWSR retail price classifications minus an average 30% retail markup to arrive at distributor price classifications across each premiumization tier.

“While inflation continues to cut into consumers’ discretionary incomes, a special bottle of spirits remains an attainable luxury that brings great pleasure to many adults. Sales of luxury spirits are being buoyed by the resurgence of restaurants and bars coming out of the pandemic, as well as consumers elevating their cocktail experiences and bars at home.”

-Christine LoCascio, Distilled Spirits Council Chief of Policy and Strategy.

Wine & Spirits Premiumization Tier Trends

Premiumization isn’t interchangeable across each market. How retail buyers purchase in metro areas versus rural areas depends greatly on local economics, consumer demand, individual target markets and retailer type (independent, mid-market, enterprise).

For example, across the spirits category, the average order in rural areas contained more standard and premium spirits than in metropolitan areas, whereas the average order in metropolitan areas contained a higher percentage of super-premium and ultra-premium spirits.

A similar but shifting trend is seen across the still wine category. The average order in metropolitan areas contained higher amounts of super-premium and ultra-premium still wines whereas the average order in rural areas contained higher percentages of value, standard and premium still wine.

Across the Champagne category, the average buyer in metropolitan areas and rural areas purchased champagne products similarly with slight variations on either side.

Premiumization Tier Trends By Metropolitan Vs Rural